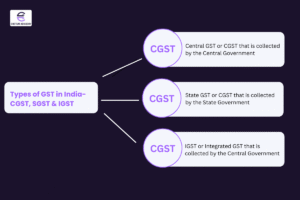

Types of GST in India: CGST, SCGST and IGST

Goods and Services Tax (GST) in 2017. One of the most significant reforms that has occurred in India. It simplified the system of indirect taxation in India. It combined various taxes like VAT, service tax, excise duty, and other taxes under one umbrella, thus guaranteeing transparency and ease in conducting business. Nevertheless, the nature of the GST in India, CGST, SGST, and IGST, continues to confuse many businesses.

This blog discusses the GST structure in India, when each is applicable, and how GST work in India.

1. Knowledge of GST Types in India.

India has a dual GST system, that is, the Central and State Governments impose taxes on the same transaction. This system will provide fair distribution of tax revenue between the Centre and the States.

“There are three types of GST in India — CGST, SGST, and IGST — each applicable under specific conditions and GST tax rates in India, depending on whether the transaction is intra-state or inter-state.”

There are three primary types of GST in India under this model:

GST types explained:

- CGST (Central Goods and Services Tax)- levied by the Central Government.

- SGST (State Goods and Services Tax) – charged by the State Government.

- IGST (Integrated Goods and Services Tax) – imposed by the Central Government on the inter-state transactions.

- Both forms of GST are imposed according to the character of the transaction, which occurs in the Centre and the states.

2. CGST -Central Goods and Services Tax.

CGST applies to the intra-state supply, i.e. when sales of goods or services are made within the same state.

Key Features of CGST:

- Applicable to intra-state sales.

- The tax revenue is raised by the Central Government.

- Companies are entitled to receive the Input Tax Credit (ITC) on the CGST paid on purchases.

- Comes Under the Central Goods and Services Tax Act, 2017.

3. SGST- State Goods and Services Tax.

The respective State Government imposes SGST on the same intra-state transaction where CGST is imposed. The SGST revenue is directly directed to the State Government in which the sale is made.

Key Features of SGST:

- State Governments collect on intra-state supplies.

- Allows ITC adjustment within SGST liability only.

- Secures states to get GST revenue.

- Comes under the State Goods and Services Tax Act 2017.

4. IGST- Integrated Goods and Services Tax.

IGST is applied in relation to the inter-state transactions whereby the goods or services are rendered out of one state to another, or in the instance of imports and exports.

IGST is collected by the Central Government, and it is subsequently shared between the Centre and the destination state (where the goods or services are used).

Example:

IGST is levied in case a business in Gujarat sells to a customer in Karnataka. Assuming that the rate of GST is 18 per cent, the seller will set the 18 per cent IGST, and the government at the Central level will then rebate a percentage of that to Karnataka.

Key Features of IGST:

- Imposes IGST on inter-state transactions and cross-border supplies.

- Gathered by the Central Government and issued subsequently.

- Promotes the free flow of Input Tax Credit between states.

- Comes under the Integrated Goods and Services Tax Act, 2017.

6. Difference between CGST, SGST, and IGST

“Understanding the applicable CGST, SGST, and IGST rates helps businesses calculate tax correctly and ensure proper credit utilization while filing GST returns.”

| Basis | CGST | SGST | IGST |

| Authority | Central Government | State Government | Central Government |

| Applicable On | Intra-state transactions | Intra-state transactions | Inter-state transactions & imports/exports |

| Credit Utilization | Against CGST or IGST | Against SGST or IGST | Against IGST, CGST, or SGST (in order) |

| Revenue Distribution | To the Centre | To the State | Shared between Centre & Destination State |

This system will provide smooth access to credit and will not have a cascading effect of taxes, as was the case in the old regime.

Read Our Related Blog- GST Registration Process in India

6. How CGST, SGST, and IGST Work Together

In the case of intra-state supplies, the CGST and the SGST would be imposed altogether; half the tax revenue would be charged to the Centre and the other half to the State.

In the case of inter-state supplies, IGST supersedes CGST and SGST, making the credit mechanism easy and also providing a harmonised tax structure in India. This built-up system enables businesses to benefit from ITC across state lines without undergoing various tax obstacles.

7. Input Tax Credit Under GST

The mechanism of the Input Tax Credit (ITC) under GST is one of the biggest advantages of GST and helps to avoid double taxation. Businesses are in a position to claim the tax paid on the purchases and deduct it against the output tax liability.

As an illustration, when a firm purchases raw materials of value 1,00,000, with GST 18,000, and finishes producing with a value of 2,00,000, with GST 36,000, it can deduct ITC 18,000 and pay only the net amount 18000.

The ITC management and reconciliation should be carried out properly to keep the compliance and prevent penalties in case of audits.

8. GST for Inter-State and Intra-State Supplies.

- Intra-State Supply: CGST + SGST

In case the seller and the buyer belong to the same state. - Inter-State Supply: IGST

Where the buyer and seller are not in the same state, or in cases of imports/exports.

This difference is important to understand as it enables businesses to pay the right type of GST and make correct returns.

9. The Role of Expert Advisory: GST Compliance.

Being a compliant entity in the GST is not just a matter of submission of returns. Businesses must ensure:

- On-time registration and filing of returns (GSTR-1, GSTR-3B, etc.).

- Right classification of goods/services.

- Reconciliation between ITC and outward supplies.

- Audit-ready Keeping records.

How Cretum Advisory Gonna Help you?

Cretum Advisory makes the process much easier by having a professional GST compliance services that will ensure GST registration and filing and obtaining a refund are done correctly and your business remains business-oriented and audit-ready.

The Final Thought

The GST system in India, consisting of CGST, SGST and IGST, has simplified the country’s complicated indirect tax scheme by combining several taxes under one umbrella. The multiple taxes are being applied within one homogeneous regime – Consolidated Goods and Services Tax (CGST) and State Goods and Services Tax (SGST) to intra-state supplies and Integrated Goods and Services Tax (IGST) on inter-state and cross-border supplies.

The framework allows tax credit to flow seamlessly between states. Understanding these elements, along with the applicable GST tax rates in India, help businesses comply with reporting, reduce costs, and maintain cash flows. Through proper filing, regular reconciliation, and professional GST compliance services, businesses can operate in this efficient and transparent tax environment with confidence.

Frequently Asked Questions (FAQs)

1. What are the GST types in India?

CGST, SGST and IGST are the three types. CGST and SGST are imposed on intra-state sales, whereas IGST is imposed on transactions between states or internationally.

2. What is the distinction between SGST and CGST?

The Central Government and the State Government collect CGST and SGST, respectively. They both are levied on the sales within a state but sent to separate authorities.

3. When does IGST apply?

IGST is used in case the goods or services are transferred between states or across borders (exports and imports).

4. How are these taxes imposed together: CGST, SGST and IGST?

CGST and SGST would be used together in the case of intra-state supplies, whereas IGST would be used in inter-state cases to enable a smooth transfer of tax credit.

5. What can companies do to make sure that GST is done?

ITC can be reconciled regularly, and returns submitted on time by keeping records. By collaborating with Cretum Advisory, the end-to-end compliance by means of expert guidance and technology-supported assistance is smooth.